How to Build a High Conviction Bond Portfolio

High Conviction is about much more than having confidence in your investment decisions.

At TwentyFour, we see high conviction as a style of active management – building a relatively concentrated and flexible portfolio using rigorous expert research while seeking material outperformance against the benchmark compounding year after year.

In our view, at any one time a true high conviction bond portfolio will typically hold fewer than 200 line items. But an unconstrained fund with a mandate to invest across the global fixed income markets has over 26,000 different securities to choose from, with a face value of over $50 trillion.1

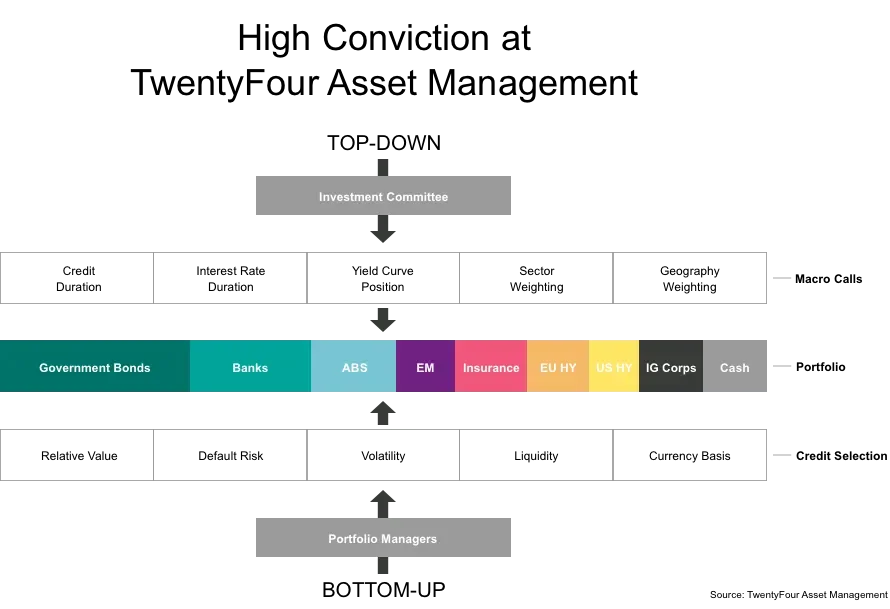

How can we be sure we are using the best sources of fixed income risk, in the most efficient way, in order to maximise performance for our clients? We start by ensuring high conviction thinking runs right through our investment process – from our top-down approach, where our biggest macro calls are made, through to our bottom-up credit work where we aim to squeeze optimum value from more micro investment decisions; which geography, sector, issuer or class of security can offer the best risk-adjusted return potential.

The Top-Down

At TwentyFour, high conviction begins at our monthly Investment Committee, which analyses market conditions, global economic data, central bank policy, as well as geopolitical risks and many other inputs, before setting dynamic allocations to a set of macro risk buckets.

These are the building blocks of a portfolio, the key risks we look to harness to give a portfolio the characteristics we feel are appropriate for current market conditions and anticipated future developments.

Once we have determined what we believe to be the optimal allocation for each of these macro calls – credit duration, interest rate duration, yield curve positioning, and geography and sector weightings – we look to implement these top-down investment biases across the firm’s relevant strategies.

These are the strategic decisions a high conviction manager can make that index-trackers simply cannot.

The Bottom-Up

After top-down asset allocation, it is up to each strategy’s investment team to populate the macro risk buckets for each portfolio.

This is where our portfolio managers decide to invest in one bond over another. If we like a sector, which issuer do we want to invest in? If we like an issuer, do we want to be in their three-year bonds or their five-year bonds? If we like their five-year bonds, are we confident they represent relative value against five-year bonds of other issuers, and could we seek to capture additional alpha in a different currency?

As fixed income specialists, this is where we believe we add a lot of value for clients. The global bond market is a large, diverse and often complex place to invest, and thus it frequently throws up idiosyncrasies and value opportunities that may only be available to those with the resources dedicated to spotting them.

TwentyFour’s investment team has deliberately been built to include a range of sector and geography specific expertise, enabling our portfolios to hold more meaningful positions in markets such as asset-backed securities and bank capital, where we believe we are well placed to capture superior yields for clients because of the time and resources we dedicate to being comfortable with the associated credit risks.

The Principles of High Conviction

We firmly believe it is the combination of these top-down and bottom-up approaches that can yield measurable differences between high and low conviction portfolios. But what are they?

Concentration – At TwentyFour we prefer to limit our portfolios to 100 or so line items. A bond portfolio must have enough diversification to tackle individual default risk, but we believe to have all-round high conviction a manager must have relatively few positions. In our view, a manager running a highly diversified strategy, or a portfolio so large they are compelled to own a large portion of the market just to stay fully invested, has given up on capturing alpha for clients through bottom-up credit work.

Specialist research – High conviction managers are typically specialists who target areas of the market where rigorous research can be well rewarded. High conviction to us does not mean high risk. It means deploying our specialist knowledge in a way that is able to generate extra alpha, or more consistent returns, without taking a lot more risk. Good long-term managers can deliver the returns investors are looking for without giving them significantly more volatility, which we would expect to eventually show through in a highly diversified strategy because at times the market will be expected to suffer widespread weakness.

Flexibility – A high conviction fixed income strategy should be highly nimble in order to take advantage of emerging value opportunities as quickly as possible. We believe this is particularly important in an asset class facing secular risks as fixed income is today, with investors facing a deteriorating credit cycle and increased uncertainty around global monetary tightening. A nimble manager can limit downside exposure while looking to exploit the few remaining pockets of value to boost returns.

Consistency – Consistency in approach should lead to consistency in performance, throughout the economic cycle. This is because a high conviction strategy should be positioned to avoid most of the risks amid weak market conditions, and capture most of the gains when sentiment is more positive. This requires the strategy to sometimes take on less risk, and play for lower returns while market conditions mean risk is generally being poorly rewarded. Naturally the opposite should apply when risk is expected to be better rewarded.

1 Based on The Bloomberg Barclays Multiverse Index, a widely used proxy for the global universe of fixed income most passive funds will allocate to. Figures as of May 2019.